Risk Parity is a sophisticated form of return layering, where the focus is not just on the sources of return but also on balancing risk across various asset classes within a portfolio. Here's how Risk Parity can be seen as a return layering technique:

1. Diversification as the Base Layer:

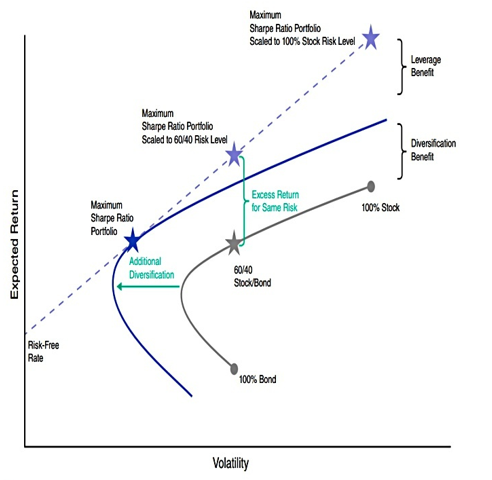

The foundation of Risk Parity is diversification across different asset classes such as equities, bonds, commodities, and sometimes even real estate or alternative investments. Each asset class contributes to the portfolio's return in its unique way, be it through capital appreciation, interest income, or commodity price movements. However, unlike traditional portfolios where allocation might be based on market capitalization or expected returns, Risk Parity focuses on equalizing risk contributions.

2. Risk Balancing as the Second Layer:

Instead of allocating capital based on expected returns or market size, Risk Parity allocates assets based on their volatility or risk. This means that riskier assets (like equities) might have a lower allocation in terms of capital but contribute equally to the portfolio's overall risk profile. Conversely, less volatile assets (like bonds) might have a larger capital allocation but still contribute equally in terms of risk. This layer aims to ensure that no single asset class can disproportionately affect the portfolio's performance, smoothing out returns and potentially reducing drawdowns during market stress.

3. Leverage as the Third Layer:

To achieve target return levels when risk is more evenly spread among lower-risk assets like bonds, Risk Parity often employs leverage. This means borrowing to invest more in assets than one's actual capital would allow, which can amplify returns from all asset classes. This layer adds another dimension to return generation, aiming to enhance yield while maintaining the risk parity structure. Here, the key is to use leverage judiciously to match or exceed traditional equity-only portfolios' returns without taking on disproportionate risk.

4. Dynamic Rebalancing as the Fourth Layer:

Risk Parity portfolios need regular rebalancing to maintain the desired risk levels across all assets. This dynamic adjustment can act as a return layer by capitalizing on market movements. For instance, selling assets that have appreciated (and hence increased their risk contribution beyond the intended parity) to buy more of those that have depreciated (and are thus underweighted) can generate returns through market timing, albeit in a systematic, rules-based manner.

5. Asset Correlation Management as the Fifth Layer:

By understanding and managing how asset classes correlate with each other, especially in different market conditions, Risk Parity can further layer returns. In stable times, these correlations might be low, providing diversification benefits. However, during market stress, correlations can rise, and here, the strategy's design to have balanced risk contributions can help mitigate the impact of any single asset class's downturn, potentially preserving capital or even generating returns through relative performance.

Implementation Example:

Portfolio Composition: 50% in bonds, 30% in stocks, and 20% in commodities, but with leverage applied to match risk levels across these assets.

Outcome: In a scenario where stocks fall but bonds and commodities hold or rise, the portfolio might see less volatility compared to a stock-heavy portfolio, providing a smoother return profile. The leverage amplifies returns from bonds and commodities, which might not have been as significant without it.

Risk Parity, therefore, layers returns by diversifying across assets, balancing risk, leveraging to enhance returns, dynamically rebalancing, and managing asset correlations. This approach aims to achieve a more consistent return stream over time, with potentially less volatility than traditional portfolios, embodying the essence of return layering through sophisticated risk management.

Precedent Investors apply an adaptation of this sophisticated technique to global equities - to either target lower risk but with the same return as global equities, or the same risk as global equities with a higher return.